Weather vs. Climate

VIPs

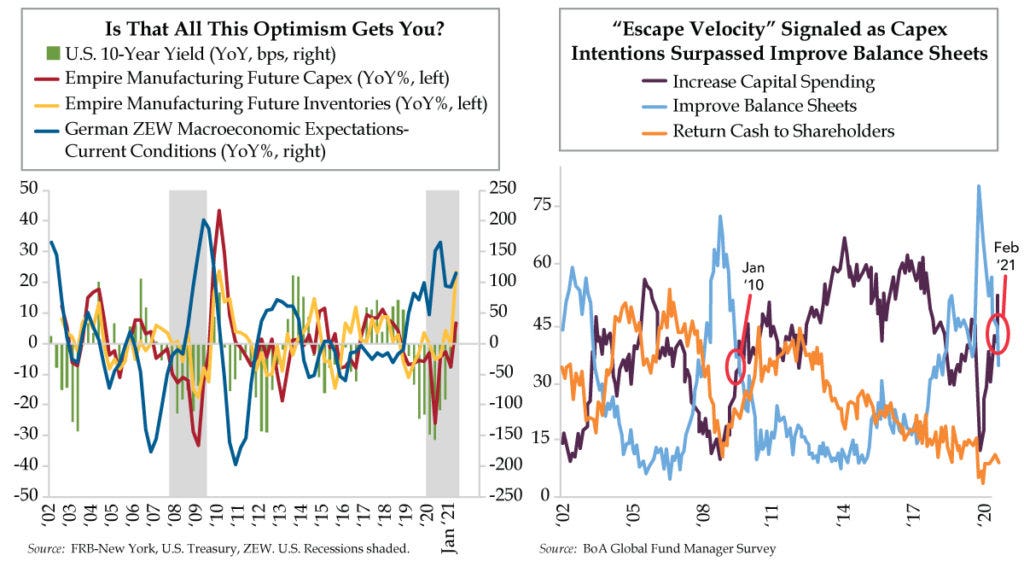

Per the New York Fed’s Empire Manufacturing survey, Future Inventories expanded rapidly in February, posting a 1.85 when normalized as a z-score; Future Capex also advanced to pre-COVID levels fo…

Per the New York Fed’s Empire Manufacturing survey, Future Inventories expanded rapidly in February, posting a 1.85 when normalized as a z-score; Future Capex also advanced to pre-COVID levels fo…