The Good Troll

The Good Troll

VIPs

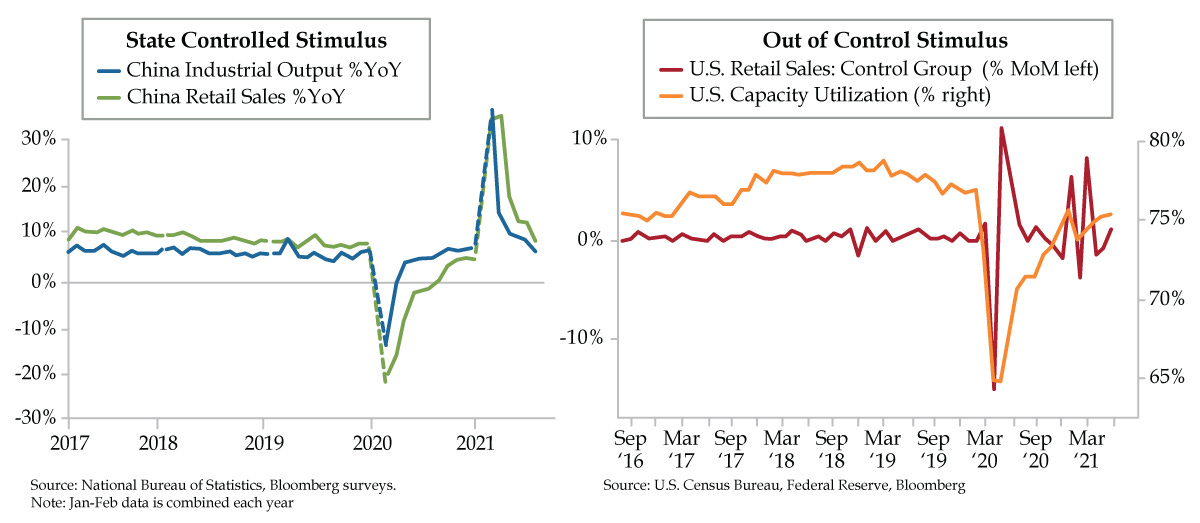

Both Industrial Output and Retail Sales in China missed expectations in June, reverting to their pre-pandemic trend; despite East Asian suppliers seeing a Delta-driven slowdown, both consumption and the factory sector bounced back in July in China, per China Beige Book

The Bloomberg consensus has today’s Retail Sales print falling 0.2% after June’s 0.6% MoM gain; while Amazon Prime Day could cause a seasonal skew, Bank of America credit card data shows services spending has fallen to a 2-year growth rate of 5.7% vs. late June’s 14.6%

Capacity Utilization in the manufacturing sector is expected to match June’s 0.3% bump and rise to 75.7% in July; however, utilization remains below February 2020’s 76.3% and has not been north of 80% since 2008, a sign of the U.S.’s underperformance relative to China

So high were the wind and waves, there would be no sinker-leaded fishing lines dropped to lake bottoms with tantalizing earthworms attached to lure the pickerel. The winds were too brisk to cast for smallmouth bass with live Golden Shiners as bait. And so, we trolled with a lure…apparently in the right spot. Per the State of Maine Department of Inland Fisheries and Wildlife, “West Grand Lake, another original home of landlocked salmon, may rightly be said to offer the best salmon fishing in the world.” Though we’d no intention of catching a landlocked salmon, my destination this past Sunday, my last day of Camp Kotok, just so happened to be the 15-thousand acres of West Grand. Had the landlocked salmon, cut off from the sea by glacial movements before humanoids roamed, been the goal, I’d have best arrived right after ice-out, between early May through June.

Luckily, my guide J.R. recognized the potential of the huge temperature swing cooler and wild winds that might lure the salmon up from their deep, cold holes. An hour in, moving at 2.5 mph in his canoe, trolling through the whipped-up waves, a bite! A lot of reeling later, there it was, silvery and spunky – a 20-inch, 3-pound beauty, a first for yours truly and plentiful enough for an appetizer to feed the 15 of us who remained. Gathered on the deck of Leen’s Lodge, we’d convened to debate the fate of the dollar on the 50th anniversary of the Nixon Shock.

While we disagreed on the dollar’s fate, we concurred that the U.S. weaponizing the greenback in the half century since Nixon dropped the gold standard exploited our position to grow our economy and its debts, in that order. Contrasting one hellacious decade of inflation against 40 ensuing years of prosperity seemed a good outcome, that is, if you set aside the worst inequality in U.S. history, a byproduct of the inability to temper greed.

If, as the majority present posited, inflation persists and worse, growth slows, what will become of the U.S. economy? Most agreed the Federal Reserve has committed a policy error by facilitating another housing bubble. Soaring home prices gave the Fed cover to exit MBS purchases while continuing to grow those of Treasuries. Even as the reopening impulse ebbs -- and in some cases reverts -- easing price pressures where they’d spiked, “transitory” won’t describe housing inflation when it manifests in the consumer price index.

As for the cyclical economy, we shared growing concerns of emergent margin squeezes given the renewed slowdown among Delta-crippled East Asian suppliers to the U.S. and exacerbating strains on already acute shipping delays. As if on cue, fresh data out of China validated the angst. Both Industrial Output (blue line) and Retail Sales (green line) missed expectations in June. Looking past the headline, today’s left chart reveals it’s nothing more than a reversion to the pre-pandemic trend in both metrics.

Indeed, a more up-to-date check via QI colleague Leland Miller of the China Beige Book (CBB) suggests both consumption and the factory sector bounced back last month. Per the CBB’s latest, “The (Chinese Communist) Party will see July as a success in Manufacturing and Services, with worries about stocks minor in comparison.”

It is interesting that the Shanghai index has stabilized, Chinese companies listed in the U.S. continue to make new lows, unable to shrug off China’s crackdown. On a fundamental level, evidence of the lingering pandemic, to say nothing of the protracted slowdown which pre-dates COVID-19, is in its credit markets. As noted by the CBB, despite the decline in rejections, July loan applications and pent-up demand declined further from the second quarter’s record lows.

In the U.S., July Retail Sales and Industrial Production (IP) are released before today’s market open. The Street is expecting a give-back in spending. The Bloomberg consensus has headline Retail Sales falling 0.2% after June’s +0.6% read. We depict in today’s right chart the Control Group (red line), which nets out gasoline, auto and building material sales and feeds GDP. After popping 1.1% in June, it too is expected to print at -0.2%.

The big technical that could swing seasonals is Amazon’s Prime Day, which landed in late June this year instead of its typical mid-July. Beyond that, based on its debit and credit card data, Bank of America has seen services spending slump to a 2-year growth rate of 5.7% vs. late-June’s high point of 14.6%. On that same basis, durable goods spending has slumped to nearly a third of its peak pace.

As for the factory sector that led the recovery, rather than focus on IP, which is all over the map due to the influence semiconductors are exerting on the auto sector, our focus is Capacity Utilization (orange line), the truest gauge of the robustness of a cyclical recovery. In July, the consensus is expecting to see a repeat of June’s 0.3% pop to 75.7%. It’s no coincidence IP peaked at the same time as Dr. Copper, which topped out on May 11th and has since fallen 12%. Who knows when we’ll get back to February 2020’s 76.3%? More unsettling: 2008 was the last time we the U.S. had a Capacity Utilization rate north of 80%. The last of us at Camp Kotok also agreed that it’s incumbent upon U.S. policymakers to reclaim our squandered outperformance to China before it’s too late.