The Daily Feather — I Need an Intern Who Can Type Fast

The Daily Feather — I Need an Intern Who Can Type Fast

There was electricity in the air. The Iraqi invasion of Kuwait fell on Thursday, August 2nd. The Black Swan event that set off a rout in the U.S. Treasury market followed, on Monday, August 6th. In three trading days, the price of crude oil jumped 30%. The long end of the Treasury curve was especially sensitive to the oil price spike sending the yield on the 30-year bond soaring; it rose 10 and 9 basis points (bps), respectively, on August 2nd and 3rd; it vaulted up by 27 bps by the 6th. Equivalent to a +4.2 daily z-score, it still stands as one of the largest one-day increases on record. QI’s Dr. Gates was jolted from his quiet economics desk solely by virtue of his two years of typing class in Junior High. Tasked by Carroll, McEntee & McGinley’s government traders, along with someone from the IT department, he manually punched in bond prices in units of thirty seconds (1/32) into the firm’s mainframe such that the govie desk could have new trading sheets to clear trades.

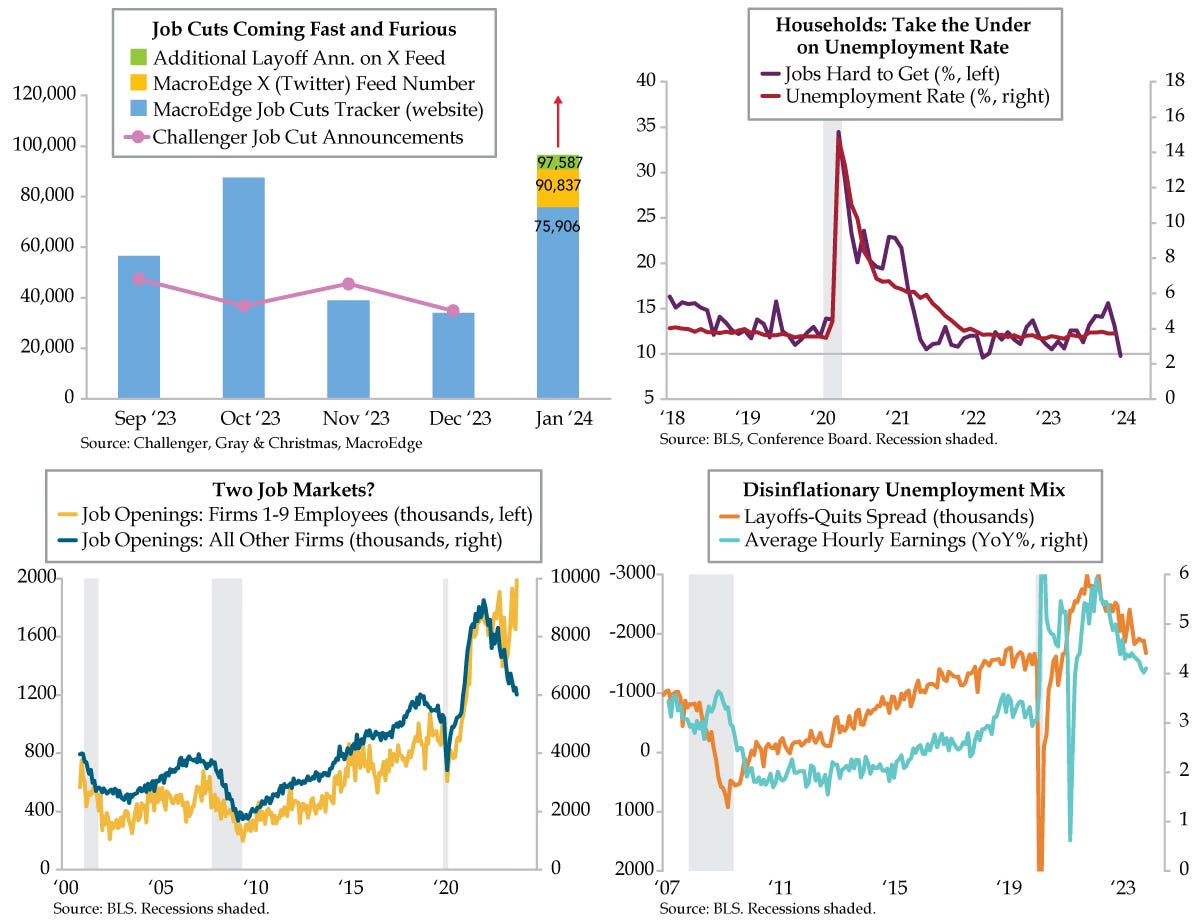

Gates went through three iterations of mainframe updates; each time, the market moved faster, and prices on the screens jumped off the page. This month, job cuts from a new source – MacroEdge – have moved in similar lightning-fast fashion.