The Daily Feather — An Open Letter to HUD Secretary Scott Turner

Dearest Secretary Turner,

Bravo on your strong stance as you take the reins of the U.S. Department of Housing and Urban Development, the entity mandated, as you noted this Tuesday, with “fulfilling its mission of providing access to homeownership.” What a noble post indeed, to ensure accessibility to all U.S. workers trying to climb the ladder at the top of which is the attainment of the American Dream. To quote you yet again, I could not agree more that providing access to insurance on loans made by Federal Housing Authority-approved lenders should be limited to those “who play by the rules and work hard.” And it’s right and true, as you say, “to end the wasteful misappropriation of taxpayer dollars.” My hat tip to you, kind sir, for ensuring that, “the entire government works together to identify abuse and exploitation of public benefits.”

To that end, as I am sure you are aware, on June 28, 2024, the Supreme Court overturned its landmark 1984 decision in Chevron v. Natural Resources Defense Council, known as the Chevron doctrine. Under that doctrine, if Congress has not directly addressed the question at the center of a dispute, a court was required to uphold the agency’s interpretation of the statute as long as it was reasonable. As I am sure you also know, in a 35-page ruling by Chief Justice John Roberts, the justices rejected that doctrine, calling it “fundamentally misguided.” The reasoning was grounded in an overreach that violated our founding fathers’ Checks and Balances apparatus. Specifically, as reported by SCOTUS Blog, as Roberts explained in his opinion, “Chevron is inconsistent with the Administrative Procedure Act (APA), a federal law that sets out the procedures that federal agencies must follow as well as instructions for courts to review actions by those agencies. The APA, Roberts noted, directs courts to ‘decide legal questions by applying their own judgment’ and therefore ‘makes clear that agency interpretations of statutes — like agency interpretations of the Constitution — are not entitled to deference.’ Under the APA, Roberts concluded, ‘it thus remains the responsibility of the court to decide whether the law means what the agency says.’”

The good news, Secretary Turner, is that you are in a position to make good on your word to “end wasteful misappropriation of taxpayer dollars” and cleave to the Supreme Court’s overturning of Chevron. The ‘why’ is simple. Your agency, under the prior administration, perfectly represents the agency overreach that’s made a mockery of Checks and Balances. In the aftermath of the Great Financial Crisis (GFC), loss mitigation required documentation and underwriting to be performed before a borrower could be approved. The absence of underwriting standards in the Covid era equated to “zero skin in the game.” No action on the part of the borrower gifted borrowers a 40-year modification or partial claim offer in the mail, or both. The ability to take up to 30% of principal balance and defer it meant that those with higher-balance loans had significant runway to “extend and pretend.” Unlike post-GFC workouts, absent was any concern for ability to repay.

On February 23, 2024, the Wall Street Journal broke the story: Biden’s Mortgage ‘Relief’ Fuels Higher Housing Prices.” As synopsized, “It has created another subprime housing bubble and put taxpayers at risk. Trump should end it.” The article succinctly captured the fraud that’s has been documented and perpetrated on the U.S. taxpayer in Covid’s aftermath: “Of the 52,531 FHA loans last year that went seriously delinquent within their first year, only nine resulted in foreclosure.” To add insult, in a genius partisan maneuver, four days before Trump was inaugurated, the Biden administration extended this de facto fraudulent mortgage modification scheme for an additional 10 months, at which time foreclosures would kick in at the start of the Midterm election year.

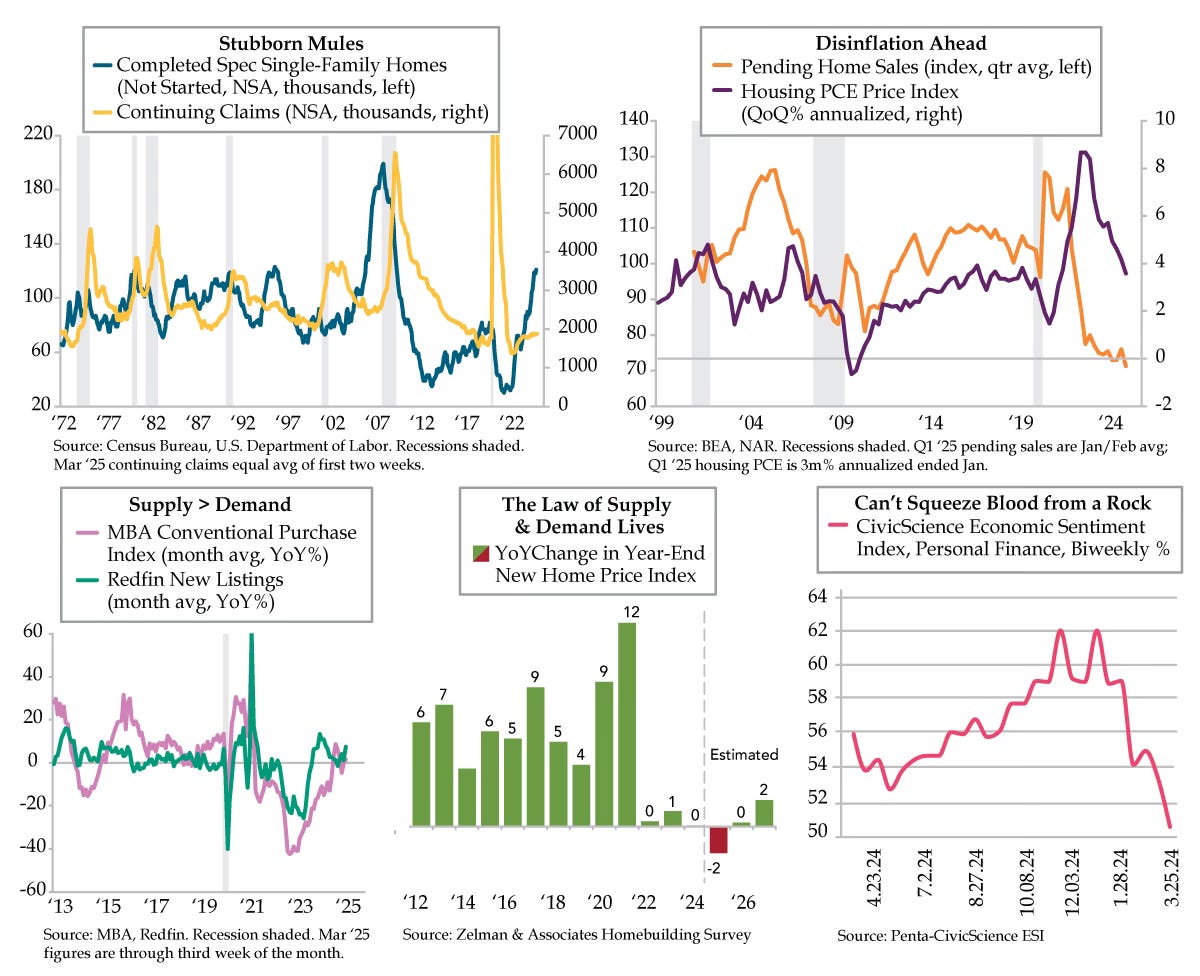

With the aid of some graphics to better illustrate, you may be asking: “Into what environment will incensed constituents finally begin to experience foreclosure?” As of the latest data, spec home inventory is at its the highest since July 2009 (blue line). The historical relationship between continuing jobless claims (yellow line) and spec home supply is plain – the number of jobless claimants has tended to play a mean game of catch-up. This stands to reason as the economy “transitions” from an era of wasteful spending to a more rational state. And as you well know, in downturns, the strongest lever on the housing market is not mortgage rates, but rather incomes. Given the current path of home prices (purple line), they too will catch down to the prevailing trend in pending home sales (orange line). Existing home inventories will also play their part as they rise beyond their seasonal norms into this critical spring selling season. As Redfin reported yesterday, “New listings of homes for sale are up 7.5% year over year (YoY), the biggest increase so far in 2025 (teal line).” And while we can hope that fence-sitters have the wherewithal to seize the opportunity of fresh supply, applications for conventional mortgage purchases are up only 1.6% YoY and have only been above water one month this year (lilac line).

At work as two-thirds of Americans anticipate a rising unemployment rate in the coming year is recession, a fact of life this administration will have to contend with, and I do hope that it is handled as well as when President Ronald Reagan first came into office in 1981. With recession, though, opportunity always emerges. As my friend since my days at Credit Suisse, Ivy Zelman, predicted yesterday, it will help the plight of many Americans seeking the dream of homeownership that new home prices are set to fall this year: “As we consider a softer-than-expected start to the selling season combined with continued accumulation in spec inventory, we now anticipate net new home prices to decline 2% in 2025 (red bar).” With luck, the current downturn in the U.S. economy can be swiftly resolved, reversing the decline in U.S. households’ expectations for the prospects of their Personal Finances (fuchsia line).

The hastiest return to a prosperous America can be secured by honest discourse with its citizens. I might humbly suggest, Secretary Turner, that you take inspiration from my dear friend Melody Wright, a mortgage expert who has tirelessly crusaded for this FHA-funded racket to be shuttered: “In future years, when financial historians discuss this FHA episode, otherwise known as government subprime, and the speculators who utilized this program fraudulently, you will have a starring role. From those who lied on their application claiming intent of owner occupancy to benefit from lax credit and downpayment requirements for their passive investment play, to those who dishonestly availed themselves of the unprecedented and generous relief options -- a’ la “the gravy train” -- this program, more than any other, has propped up nose-bleed home prices. Tightening program standards and punishing those who abuse them would immediately result in true price discovery in many markets. We can only hope and pray that the current administration will have the political will to root out the systemic fraud and stomp it out. Perhaps then our younger generations might have a shot at achieving the ever-ephemeral American dream.”

Secretary Turner, your vigilance in attacking this effective taxpayer embezzlement will secure your place in the history books of government reformers and stand forever as an example to those who follow in your footsteps. Housing should not be the sole purview of the privileged few, but rather attainable by all who endeavor to provide financial stability and a roof over the heads of their families. The time is nigh for you to stand proudly in the name of hardworking American men and women who play by the rules and work hard.

Sincerely,

Danielle DiMartino Booth, writing humbly on behalf of We the People

THANK YOU!

Just an amazing letter!