Mobile Army Surgical Unit

Writing the Weekly Quill is akin to embarking upon an ocean journey with no compass and the sole knowledge that the data determine the point of disembarkment. Wednesday evenings thus leave me excited to have arrived at my destination…late at night. The silver lining is happening upon old friends while trying to unwind. Last night, it was M*A*S*H., the movie. If you’ve seen it, you’ll understand why, released nine months before I was born, it was no mainstay in my upbringing. Because ‘R’ ratings no longer impede, I assure you perfect casting and directing pulled off the blackest of humor. The unlikely backdrop of a bloody operating room in the Korean War produced a movie that was inducted into the National Film Registry in 1996. If you’re unfamiliar, you’ll get it when I tell you M*A*S*H could never be made today. As Pulitzer Prize winner Roger Ebert wrote on January 1, 1970, “It is the flat-out, poker-faced hatred in M*A*S*H that makes it work. Most comedies want us to laugh at things that aren’t really funny; in this one we laugh precisely because they’re not funny. We laugh, that we may not cry.”

There’s no better night than tonight to get in a good laugh. Today marks the last day of what feels like the longest stretch ever of FedSpeak before May’s Federal Open Market Committee convenes. Though nothing is on the calendar, it wouldn’t be shocking to see Powell garner another headline regaling the “very strong” U.S. economy as he references the labor market, the most lagging of all economic indicators. Or maybe we could squeeze in a “100-basis-point” bomb from Bullard for posterity. At some point, all this hawkish talk is going to give the terminal fed funds rate a 4-handle. In the meantime, Powell couched his own hawkishness yesterday with the usual -- policy will aggressively tame inflation…but always and only be made on a “meeting by meeting” basis.

If data dependency is still a ‘thing’ at the Fed, they’ll have plenty to analyze as they sip that first cup of coffee around the oval table in the Eccles Building May 3rd. Some smatterings of sentiment will hit the wires as will more damning data on home price appreciation castigating policymakers’ insistence on remaining in credit easing mode with mortgage-backed securities purchases until Quantitative Easing’s bitter end. And the first print of first quarter GDP hits next Thursday.

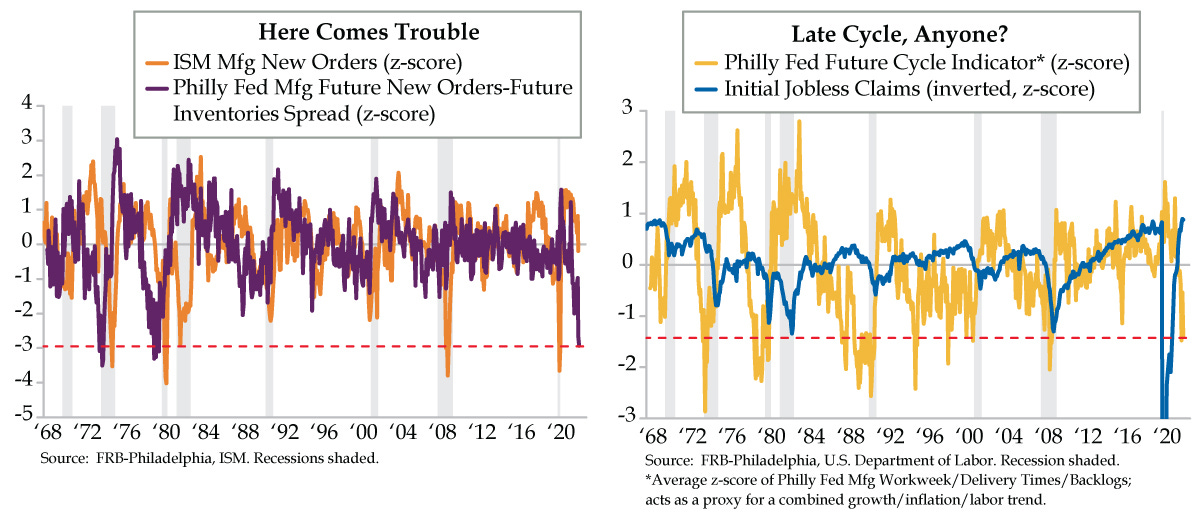

But the biggie on the ECO calendar will be the Monday before they meet. The April ISM headline is forecast to tick up to a robust 57.5 from last month’s 57.1. All eyes will be on New Orders, which unexpectedly fell by nearly eight points in March to 53.8. Factory sector data in hand suggest downside risk for this closely tracked gauge. First, we saw future inventories tank in last Friday’s Empire State print. This was followed by yesterday’s Philadelphia Fed. While most of the focus this morning was on the broader outlook sinking to the lowest since 2008, we were squarely focused on where 125 CEOs see their inventories six months hence.

At 17.3, April future inventories clocked in 13.5 points below last month’s 30.8. In the same spirit we collect the real time differential between current inventories and new orders, we can contrast that of their future counterparts. With a starting point of 22 in March to 3.7, the future new orders swing was even bigger than that of planned stock on hand. At -2.93, the gap between the two using a z-score – standard deviations from the mean adjusted for volatility – is the deepest since January 1974 (purple line). Even if the historic relationship between this gauge only loosely holds with ISM New Orders -- which as a standalone z-score in March hit -0.2, the lowest since May 2020 (orange line) -- we can reliably forecast a recessionary print in coming months.

As for the “unsustainably hot” U.S. labor market that Powell feigns keeps him up at night, he should soon be sleeping well. At -1.4, the z-score for the aggregate of future delivery times, backorders and the workweek crumbled to the lowest reading since December 2008 (yellow line), when the Great Recession was six months shy of ending. With deference to Powell, forward trumps backwards. Through the rearview mirror, the z-score of initial jobless claims of 0.88 is the second highest in data back to 1968, lower only than last month’s 0.9 print (blue line, depicted inversely).

One aside that we’ll delve into more deeply in Saturday’s Intelligence Briefing is the fine point of future delivery times as evidence mounts that freight is surreally entering a freight recession. On that note, the one single metric within the Philly Fed that swung to the greatest degree – from 39.7 to 17.9, by 21.8 points in one month to a pandemic reading – was current delivery times. The backup at the loading dock has disappeared.

We will look for further evidence of industrial recession in this morning’s S&P Global April Flash Manufacturing PMI. The headlines, however, continue to preview what’s to come. Last Thursday, the automotive components maker Tenneco announced it was laying off 648 at its Kettering, Ohio facility. And just yesterday, CJ Automotive, in the same space, announced it was closing its Butler, Indiana plant. Call this the “extra” anecdata that eventually make their way into the data, kind of like Sylvester Stallone in M*A*S*H (Google it).