Happy Gallbladder Good Health Day

VIPs

At $43,355, new car prices hit a record high for a fifth straight month in August, per Cox Automotive, up nearly 10% from last year; sales have now slowed for four months straight, with the year’s current run rate the lowest since 2009, per the Bureau of Economic Analysis

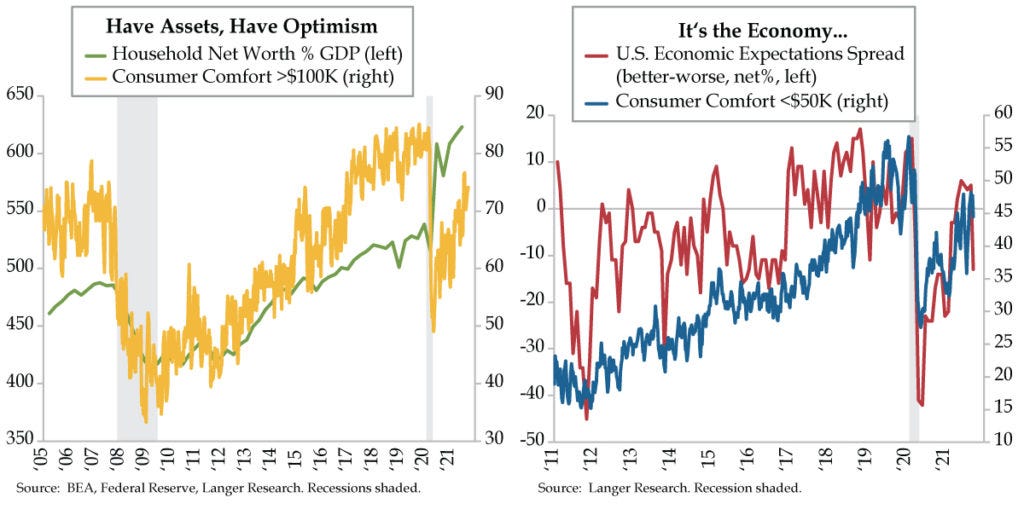

Per the Fed’s Q2 Flow of Funds, U.S. household net worth rose by $5.8 trillion to a record $141.7 trillion, or 623% of GDP; those making $100,000 or more are near record optimism, per Langer’s Consumer Comfort Index, as a result of gains in equities and real estate

In the last month, those expecting the economy to improve fell 11 points to 27%, the largest decline in 13 years per Langer; outlook for those making below $50,000 fell 16 points, with Democrats seeing a 21 point dimming in outlook vs. an 8 point decline among Republicans

For something excised as often as it is, one wonders why we even other have one. Measuring between 2.8 to 3.9 inches with a capacity of 30-50 milliliters, the gallbladder certainly qualifies as miniscule. That said, it enlarges to the size of a pear as hunger builds. Post-meal, this organ flattens as it releases bile into the small intestine to digest fatty foods. That’s not to say the gallbladder produces bile; that’s the function of the liver in the biliary tract system chain of command. Condensing bile, however, does enlist the tiny organ – the liver produces between 800-1,000 milliliters of bile daily; upon its arrival to the gallbladder, it’s concentrated between 5-18 times into compact storage. It’s this “Ant Man” like metamorphosis that’s essential to emulsify fat ready for digestion by the lipase enzyme. Let lipase run too high and risk pancreatitis or worse, kidney failure. If you’ve still got one, as so many do every September 24th, celebrate Gallbladder Good Health Day.

For all the tough talk, many investors are quietly asking why we need Federal Reserve Chair Jerome Powell telling us a taper is in the wings, and a concentrated one at that, if the deployment of a taper will negate the need to taper. Setting aside the impromptu channeling of Yogi Berra, everything makes sense about tightening inducing slowing. Thursday’s melt-up in stocks was likely tied to just this, along with one hell of a bout of short covering. Aiding and abetting are signals the economy is slowing and occurring at such a fast pace, we’re struggling to keep up.

For months now, we’ve been relaying a deterioration in buying conditions for big ticket items via the University of Michigan’s twice-monthly sentiment data. The time for the data to play catch up is apparently upon us. On Wednesday, Cox Automotive reported that at $43,355, new car prices had clocked a record high for a fifth straight month; the price is up by nearly a tenth from last August. Little wonder, car sales have slowed for four months running and are expected to maintain that slowing streak in September. The deeper context is that total sales last month were not only the lowest since April 2020 but among the weakest in a decade. Per the Bureau of Economic Analysis, the year’s current run rate is the most anemic since 2009.

The glass is half-full contingency that purports bond yields spiked Thursday cite the consistency of the improvement in jobless claims. With deference, we’ll know how the absolute recovery is panning out next week with the Department of Labor’s September 11th sum of the aggregate of claimants in to 27%, the first week that does not include the supplemental benefit programs. The last print we have from yesterday showed 8.5 million collecting through the final week. We were heartened to see 31 states, or 61% of the nation, had initial state claims that were outperforming the U.S. average, which has claims 41.4% north of where they stood in the baseline week of February 29, 2020.

Be the good news as it may, we’d prefer that the nationwide average last week was not exactly half – at 21.2% over that same date. We were also dismayed to see not-seasonally adjusted state claims (the only dataset we can use that spans the pre- and post-pandemic eras) rise by 40,307. This was the first increase in nine weeks; and at 306,209, we were also not impressed with claims’ level piercing the 300,000-mark for the first time in five weeks.

We did receive a validation of known good news with Thursday’s release of the Fed’s second quarter Flow of Funds. Fueled by a $3.5 trillion gain in the value of equities and a $1.2 trillion boost to real estate, U.S. household net worth rose by $5.8 trillion to a record $141.7 trillion or 623% of GDP (green line). Is it any wonder that after a bit of agita, those queried on a weekly basis and reported in Langer’s Consumer Comfort Index with incomes of more than $100,000 are about as optimistic as they’ve ever been (yellow line).

There is a Langer history that goes back ever farther, that of its monthly take on how the collective ‘we’ feel about our current set of circumstances and what the future holds which dates to 1985. With a hat tip to Philippa Dunne for pointing out the magnitude of the move from mid-August to mid-September, those who expect the economy to improve cliff-dove 11 percentage points (pps) to 27%, the biggest decline in 13 years. The other side of the coin is those who think the economy will weaken, which rose 7 pps to 40%. The spread between the two has caved to -13 (red line), the lowest in nine months.

Not surprisingly, the outlooks of those making $50,000 or less – the cohort most negatively impacted by the fiscal dive – tanked by 16 points (blue line). With their party publicly ripping itself apart at the seams, Democrats’ expectations fell by 21 points vis-à-vis the fall of 8 points among Republicans.

We wish it wasn’t the case, but the list goes on. While it doesn’t phase investors, Delta refuses to improve at the pace predicted by epidemiologists’ models. The household credit cycle is finally commencing as evidenced by fast-rising foreclosures. Like a gallbladder about to go bad, the junk bond market is cluing in to building stresses.