Freeze(r)-Frame

VIPs

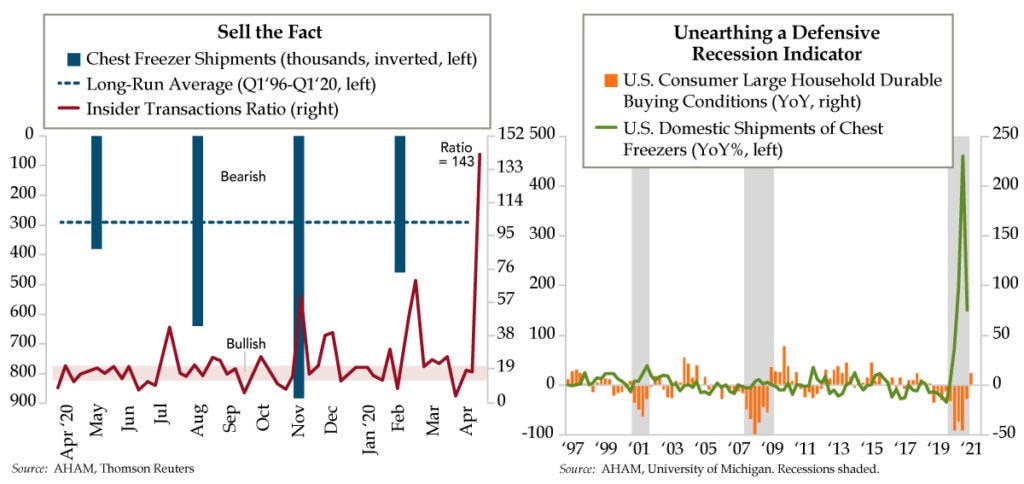

Domestic chest freezer shipments catapulted to 883,000 in Q4 2020 before leveling off in Q1 2021, vs. a long-run rate of 296,000 since 1996; these shipments have a negative correlation with large…

Domestic chest freezer shipments catapulted to 883,000 in Q4 2020 before leveling off in Q1 2021, vs. a long-run rate of 296,000 since 1996; these shipments have a negative correlation with large…