Clark Griswold’s Inspiration

Call us Thanksgiving purists. At QI, we’re deeply offended by public displays of Christmas beginning the minute the last Trick-or-Treater clears the front door. Now that it’s kosher to flip the switch, the innate historians in us wish to share the origins of outdoor lights. It started in the 17th century when Germans attached candles to trees with pins or wax. Open flames on dried trees…hmmm. Combustibility risks notwithstanding, the practice spread throughout Eastern Europe over the next 200 years. It wasn’t until 1882 that glass balls and lanterns displaced candles in full glory when the first Christmas tree lighted up in New York care of Edward Johnson, a friend of Thomas Edison. In 1903, the American Eveready company produced the first Christmas light set but they were prohibitively expensive, pushing $100 a string in today’s dollars. As for the culmination -- Clark Griswold caliber lighting -- rock star displays weren’t possible until 1927 which heralded the introduction of safe outdoor Christmas light bulbs.

After the last two weeks’ Quills on the dire commercial real estate sector, we’re viewing December as the holiday punctuated calm before the 2023 storm. We’ve only a one-month reprieve of firms reticent to reduce headcount in the holiday season. Consider the following opening line from a WCBI wire story from Belden, Mississippi that ran Tuesday: “More than 2,500 employees of United Furniture are now without jobs, just days before Thanksgiving.” Now magnify the toxic optics by substituting “Christmas” for “Thanksgiving.”

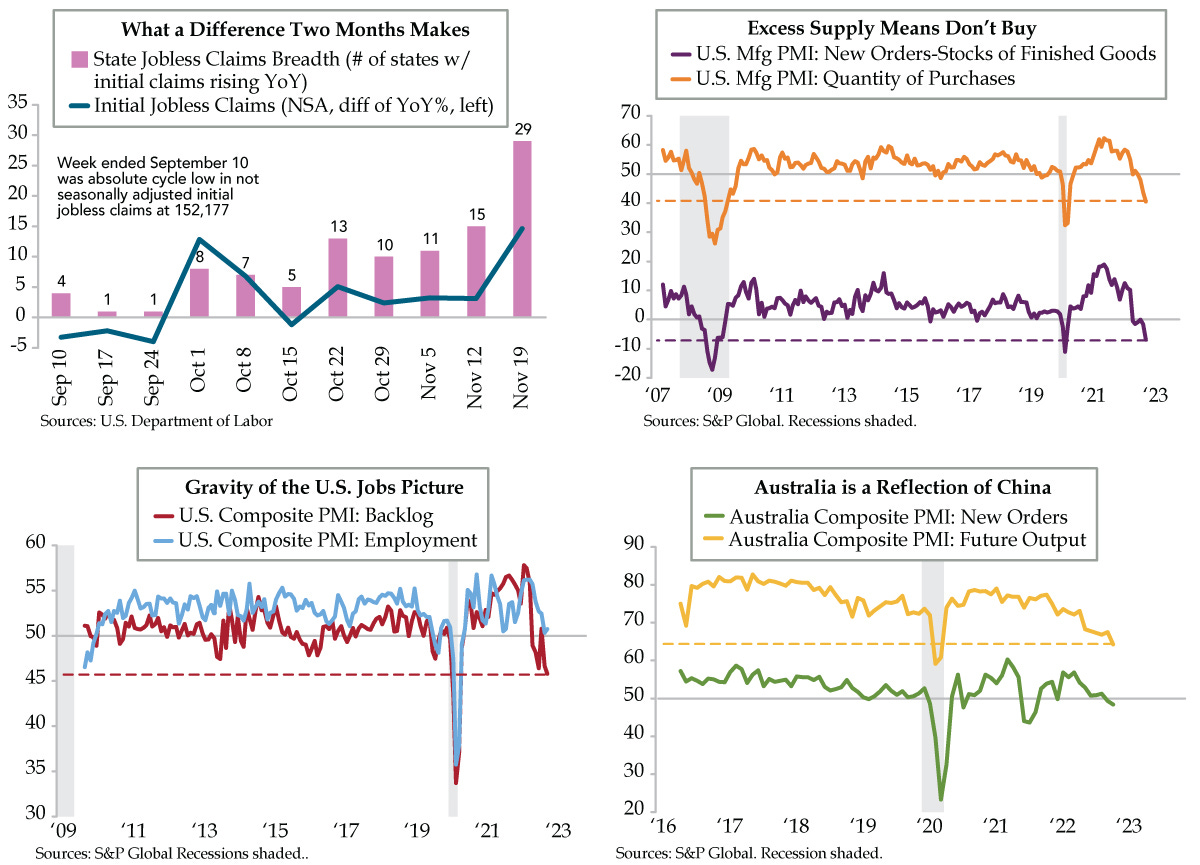

Even before the clock winds down on 2022, time is running out. The Department of Labor (DOL) reports initial state jobless claims every Thursday at 8:30 am ET for the week ended the prior Saturday. The one-day-early report released Wednesday reflected the week ended November 19th. Continuing claims lag by a week; Wednesday’s report was for the week ended November 12th. Ergo, two weeks ago, 1.551 million were collecting unemployment insurance, up by 19% since the May 21stnadir. If continuing claims in the subsequent week ago rose by the 17,000 increase in initial claims reported Wednesday, continuing claims have risen by an even 20%.

Drilling down, in the week ended November 12th, seasonally adjusted (SA) initial claims fell by 3,000 while SA continuing claims rose by 48,000, a delta of 51,000. While we can’t account for the vagaries of the DOL’s models, there’s no coincidence that continuing claims are rising at a faster relative pace. August layoffs at such companies as Walmart and Verizon have rounded the three-month severance mark. A cascade effect is forthcoming as more former employees free up to apply for unemployment insurance.

Especially in the post-pandemic era, the cleanest claims data are the level of not seasonally adjusted (NSA), a pure count. Seasonal adjustments attempt to account for sequential comparisons, they’re tricky to adjust on a weekly basis due to calendric quirks. September 10th marked the low in NSA claims (blue line). Separately, eight weeks ago, one state had initial claims rising year over year (YoY). Eight weeks later, 29 states are in that camp (lilac bars). Not illustrated is the race to rising nationwide claims. Since the low (good) point, when claims were off by 48.9% in the week ended September 24th, through the week ended November 12th, the average weekly increase in YoY claims was 4.6 percentage points (pp). In the latest week, claims jumped from -16.7% to -2.0%, a 14.7-pp delta, more than three times the pace since the weakening began.

The bottom line: By this time next week, markets will be grappling with claims being up YoY across the United States for the first time since March 2021.

Validations are multiplying. The headline S&P Global Composite (economywide) Purchasing Managers Index for the U.S. for November all but shocked the macroeconomics community Wednesday morning, printing at 46.2 vs. estimates of 48.0. This marked a fifth straight month of weakening and the second-lowest level since the pandemic first hit. More worrisome is the persistent decline in Backlogs, which peaked at 57.8 in March and have since slumped to 45.8, a deeply recessionary read (red line). Pent-up demand has segued to destroyed demand which will translate to the employment index’s imminent turn to negative territory (light blue line).

Taking the lack of pent-up demand one step further, excess supply is on display through the prism of manufacturing New Orders-to-Stocks of Finished Goods spread (purple line), something only the S&P Global PMIs can illustrate (ISM doesn’t parse the inventory pipeline from raw inputs through finished product). The current inversion is consistent with past recessions and explains why the Quantity of Purchases (orange line) has collapsed from July 2021’s peak of 62.3 to 40.8. Pandemic aside, this is the lowest print since May 2009. A sharp inventory correction looms.

Broadening out, we continuously emphasize the futility of hoping China rides to the rescue, as has been the case since the Great Financial Crisis (GFC). Given Australia’s economy is tethered to the Middle Kingdom, we can treat it as a better read than Chinese official data. Australia’s November S&P Composite PMI (data started 2016) revealed New Orders (green line) and Future Output Expectations (yellow line) falling at levels concomitant with the pandemic’s onset. Recall that Australia avoided recession in the GFC. Today’s succumbing of the economy Down Under flags the broader globality vis-à-vis the GFC. ‘Tis the season to enjoy the bright lights while we can.