Au Revoir Mes Petites

When the time came to part ways with Sister Agnes at Mount Sacred Heart, I knew well enough to say “Adieu.” Years of studying French with her as a ruler-in-hand teacher had given me such a solid foundation in that romantic language, I’d go on to win poetry awards for original work. But she and the ruler she’d rapped on my knuckles I was ready to say goodbye to forever. “Au Revoir” is what I said in my heart to my 14-year-old twins this past weekend as I hugged them one last time before leaving them at Culver Academies in northern Indiana. They are the third and fourth, respectively, to leave me with that sick feeling in the pit of my stomach. But I know the goodbye was not of the Adieu nature, what you would say to someone on their death bed or who was moving away forever…or Sister Agnes. Until we meet again, which I trust will be soon. That is what I said, in my heart, to my littles. May they acclimate quickly to dorm and barracks life and make fast friends fast.

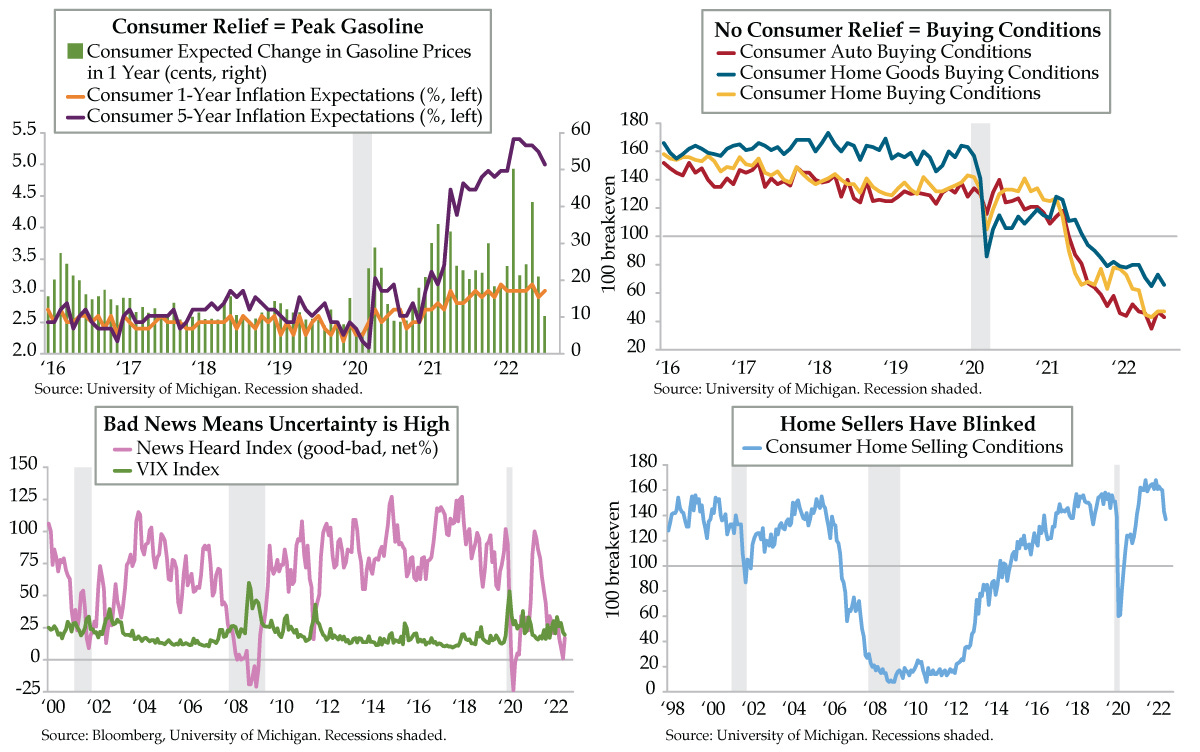

Acute uncertainty is plaguing more than my twins and me. Though off its post-pandemic trough, at 17, the net of good-bad News Heard (lilac line), is a fraction of the 100 it clocked in April 2021, when that third stimulus check was directly deposited into U.S. households’ accounts. As we saw in Friday’s preliminary read on August consumer sentiment from the University of Michigan (UMich), the inflation ignited as a result of that reckless fiscal spending has left in its wake massive anxiety. To contextualize, the average News Heard reading of 9 in the last three months has only been seen during two other episodes – right after the pandemic hit and during the Great Financial Crisis.

To be sure, gasoline prices falling to $4 from $5 a gallon are having an ameliorating effect, pulling down inflation expectations (upper left chart). And the Nasdaq being up 23%, the average bear market rally, has no doubt allayed some of households’ worst fears. The relief that the Federal Reserve’s Jerome Powell will issue a stay of execution is also evident in the VIX Index closing below 20 for the first time since December, before all this nasty monetary policy tightening business started.

While we will be the first to admit we’re wrong if Powell chokes, until then, we see investors’ insouciance as misplaced. Being the savvy politico he is, he knows the Street value of the podium at this Friday’s Jackson Hole confab. There were rumblings over the weekend that he could touch on Quantitative Tightening (QT). Reuters columnist James McGeever wrote that, “Anything Powell says about ‘QT’ and reducing the bank's near-$9 trillion balance sheet will grab a lot of attention - in part because investors and policymakers have been so vague to date on how they view the impact of such liquidity withdrawal alongside the aggressive rate-hiking campaign.”

Solomon Tadesse, head of quantitative equities strategies North America at Société Générale, concurs with McGeever. In his view, markets are not factoring in QT at their own risk. Over-tightening is a real possibility if every $100 billion in QT equates to 12 basis points (bps) of tightening, as his quantitative analysis suggests. He has told Barron’s, “It might not be totally symmetrical, but there will be a meaningful impact.”

QI Glossary: QE or QT cloud the effects of pure interest rate policy. Investors and academics endeavor to quantify the “shadow fed funds rate” to reflect what rates would otherwise be without QE or QT.

Our overly simplistic math pits the shadow fed funds rate against QT to date. At 288 bps, the rate is 58 bps north of fed funds. The $53 billion in QT to date suggests roughly 1 bp per $1 billion. Of course, there are other sources of tightening pushing this rate higher. We know from Lacy Hunt’s favored liquidity gauge – Other Deposits under “Liabilities” in the Fed’s weekly H.8 report – that liquidity peaked in March and has been coming down since then, which is quite the backdrop against which to ramp up QT to full throttle next month.

The most visible manifestation of liquidity depletion can be seen in the U.S. housing market. Inventories and “stale” listings, which Redfin defines as being on the market for 30 days or longer without going under contract, are rising at a brisk pace. In July, 61.2% of for-sale homes were stale, up from 54.4% a year earlier. According to Redfin, “That’s the first year-over-year increase in ‘stale’ housing supply since the beginning of the pandemic and close to the biggest uptick in Redfin’s records, which go back to 2012. The only time it increased more (13.9% YoY) was in April 2020, when the housing market nearly ground to a halt.” Sellers have clearly received the memo. While selling conditions remain well above normal (light blue line), they’ve gapped down these last two months to February 2021 levels. The momentum to the downside is picking up.

Per UMich, the spillover effect from Home Buying Conditions (yellow line) to Home Goods (dark blue line) is unprecedented. As one QI subscriber and furniture industry veteran noted over the weekend, “The recession is in full swing for durable goods. Trust me on that one. We’re at half of what our sales used to be. Stimulus money has dried up and the housing pullback means nobody is spending on furniture for new houses.” Ditto on the car buying front (red line), a message Detroit will get as buyers increasingly bid slick salespeople “Adieu” at the car lot.